Cuttings and Publications of Edward C D Ingram

Newspaper Cuttings and Publications

CLICK ANY FIGs TO ENLARGE -

Then page-back to return.

FIG 1 at right

This new mortgage model, born out of a need to cope with inflation, has since then been put into practice in Turkey. In opposition at the time Ted Heath, later Prime Minister, and Margaret Thatcher then shadow Minister for Housing, took an early interest.

A Cambridge economist soon picked up on the idea and said it was the best way forward in principle.

The Editor of the Building Societies Gazette, Eric Holmes, was furious that the academic had not given credit to Edward for this idea and he gave an unheard of three page spread to him and his Housing From Income Committee on the new idea that mortgages should have a link to incomes to ensure that they were affordable.

See FIG 2 below.

|

| Click to enlarge and page-back to return. This was followed by a series of articles by the committee explaining more. |

The idea was not fully developed for use in all economic conditions and it was not a simple and easy model to manage. Although it has been implemented in similar form in Turkey since then, it needed further mathematical investigation to perfect it and Edward had no time to do that till after he retired in the 1990s.

It is now being published online HERE

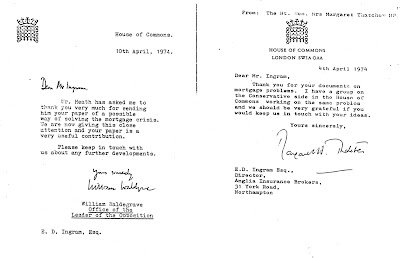

FIG 3 - Edward had appealed for funding to do this research in this letter published by The Times on 11th April 1974. He was supported by Michael Morris MP, (later Deputy Speaker in the House of Commons,and now The Lord Naseby), as seen in the quote from Hansard.

In this letter Edward warned that the current mortgage model still used today by mainstream lenders was unsafe; and so it has proved time and time again both before and since.

Many people say that the problem was sub-prime lending as if there was no property price inflation related to normal lending: as if lenders do not lend more when interest rates fall...

When the Fed had to raise interest rates to re-balance the economy in the USA in 2007/8 prime borrowing repayment costs were slated for an increase of 58%. Was that not a problem? Did it have no effect on property prices? Will it not make economic recovery difficult as QE eases and interest rates eventually do rise?

Was it not also a problem that many people had used their reserve income on credit cards and could not afford to pay more, never mind a lot more?

The solution to all of these issues can now be found on Edward's Mathematics Blogs and it is discussed here as well as A WAY FORWARD, with links to the maths, as well as the economics on this Blog called INGRAM SCHOOL ILLUSTRATIONS.

It is thought that the new design for debt and other structures will out-date the debate over Keynesian / Hayek etc debates, making economic growth into an almost natural ongoing condition - which is what both of those academics hoped to achieve, because that is what could happen if all pricing was done correctly. There would still be undulations in the business cycle but maybe not enough to justify much, if any, intervention.

However, there is still a case for tighter management of the money supply and there is a strong case for reforming the way that currencies are being priced. A third of world GDP goes through a currency price. One price cannot sensibly be used to balance both trade and investment flows. The result is a great deal of needless volatility in currency prices.

Edward has now published outline solutions to all of the above problems in his weekly column at www.fin24.com (search the site with the words "Edward Ingram" to find those essays), and Edward will publish these solutions again in his forthcoming book in respect of all of these areas of instability that are inbuilt into the structure of our economies.

Recently, in addition to the PEER REVIEWS page on the main Blog, and the support given by the likes of Graham Hollick, a past president of the International Union for Housing Finance, this press release has been sent out by a journalist, confirming this opinion: SAdly the link has been lost. Sorry.

http://www.newswire.net/newsroom/finance/74551-Mortgage-Finance-Expert-Edward-Ingram-May-Have-Solution-Global-Economic-Instability.html

OTHER ACTIVITIES

Meantime running the business was taking most of his attention because the same economic conditions that were worrying lenders were also worrying the nation's investors as shown by the 75% decline in the 30 share index.

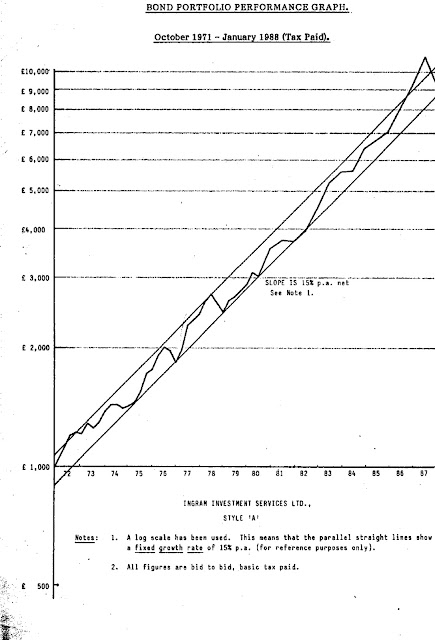

But Edward keep his own client investors safe as shown by his audited performance graph FIG 4.

But Edward keep his own client investors safe as shown by his audited performance graph FIG 4.The scale used is not an ordinary one but a log scale. This means that the straight parallel sloping lines show that the investments were growing at an almost constant 15% p,a, which is a compound rate that doubled the value every five years, net of tax and before management fees.

FIG 5 - this in-house graph showed that the performance continued for the best part of Edward's 22 years at the helm

His philosophy as he told his clients was that there is nothing wrong with being in cash.

The reason for investing is to do better only as and when we see a strong investment market rising, and we can allow risks after we have made a profit which is why we ran the gains and accepted an occasional sharp fall at the top of the market.

The reason for investing is to do better only as and when we see a strong investment market rising, and we can allow risks after we have made a profit which is why we ran the gains and accepted an occasional sharp fall at the top of the market.

FIG 6 at right shows a different type of fund management called Fund of Funds where unit trusts were used to create a portfolio. Here cash was not an option so the funds were more volatile.

Ingram's were well ahead of the World Index in the 1990s and also ahead of the UK All Share index, although the fund was aiming to do better than the World Index it also did better than the All Share Index.

FIG 7 below.

A NEW INDUSTRY WAS CREATED

So many brokers had tried to copy the Ingram method that a new industry was born to make it streamlined. It was called Broker Bonds. The Broker Bonds were funds managed by independent brokers like Ingram Investment Services Ltd, based at 83 St. Giles Street, Northampton, UK, and they rode on the back of the in-house funds / investment bonds of the insurance companies, picking the best funds and switching between them from time to time on a percentage basis.

This performance Prize Winning Institutional managed fund was the Clerical Medical fund but the Ingram Fund,using the same component managed funds in a different mix did better as shown by this independent source called Micropal.

FIG 8 needs to be clicked on to

enlarge it. And another click will make it readable.

enlarge it. And another click will make it readable.

It explains the Ingram team's investment philosophy and reports that the Daily Telegraph mentioned that they were top in the country in 1980 based on performance - again.

They had a very well established reputation and a long serving staff. One of them, David Goy, had invented a new pension product for Standard Life before joining the team.

FIG 9 - This also needs to be clicked on.

This idea was very popular with the press and the Department of Trade and Industry that was supervising the sector.

Edward got to know Garry J Heath during this time. The issue was dropped shortly after because Edward left the country for Africa but the idea has now been established at least in the UK as 'Platforms' and it in use in South Africa. It works well, speeding the process of dis-investing and re-investing money without any adviser getting access to the funds. It saves up to 30 days, taking place within one day. Interest on overnight money may be used to pay the costs.

Before the system was adopted, Garry said (rightly) that it is a far superior method of handling client's money without actually touching it than anything they have put in place in the UK since then, as at 2010.

FIG 10 Helen Pridham at Planned Savings confirmed that she had audited the Ingram fund's performance.

She later organised a competition between independent advisers that were in the field in which Ingram's came top ten times out of sixteen reports.

FIGs 11 - 12 Four of the long serving staff members (of 12 at the peak) confirmed that no client had suffered a loss in the entire history of the company as a result of following Edward's advice.

That is probably not something that any stockbroker can claim and it is not something that most advisers can claim.

Ingram's did not recommend Final Salary pension schemes despite other advisers making fortunes in commission that way. Many of them were sued for giving that kind of advice. The Shell Oil Company recorded a deficit of 131bn pounds at one time, on its Final Salary Scheme.

The Ingram team also stopped offering low cost endowments in the mid-1980s when it appeared that the investment environment and the investment management options had seriously changed, leading to doubts about future investment returns. It turned out that this decision was also correct and many banks and others that pushed their clients into these on a massive scale at about that time, later got sued for bad advice.

FIG 12 - Two other staff members, Mrs Kitchen and Felicity Prior, a fully qualified accountant, both involved with the books and accounts confirmed this.

FIG 13 Years later Philip Bailey who had left school to join the team, and was a trainee fund manager, at Ingram's kindly wrote from his new job as a fund manager for Grant Thornton. He Confirmed the facts about Final Salary Schemes.

SPORTS

Philip earned a fine reputation in International Yatch Racing as a much in demand skipper / helmsman, frequently winning or coming in the top three.

OLYMPICS MEDAL

He was also in good company because Edward's co-director Micky M Walford, an economics and sports master at Sherborne School, had played for England as Captain in the Hockey Olympics (Silver Medal), played for his County at cricket, (was an Oxford Blue who scored 212 runs against the MCC) and had played Rugby for England. He was good at tennis too. A street was named after him. The Daily Telegraph called him the Old Corinthian.

Micky never minced his words to clients, just laughing at them if they were doing something he thought was not a good idea.

FIG 14 The Times published Edward's letter defending his industry which was under attack as offering nothing of value!

He won his case, much to the relief of the institutions and everyone else involved.

But the regulators and the big brokers had the last laugh when they brought in some new capital requirements supposedly to protect clients. This put thousands of small advisers like Ingram's out of business.

FIG 15

FIG 15This is a snippet from a one page article that was written by Keith Redhead with Edward as co-author for Credit Management Magazine.

Kieth taught economics in Coventry and has published a number of books.

The idea was to unitize loans as a way of reducing the volatility of the repayments when variable interest rates were used. It can work but so far it has not been tried.

Edward has now created and published online an entirely new mathematics of safe lending for the housing industry.

Edward has now created and published online an entirely new mathematics of safe lending for the housing industry.

FIG 15a The Full page